How algorithmic DCA allocation boosted loan collections at a Tier-1 Servicer

Los inversores en NPL a menudo se acercan a la compra de carteras de préstamos con poca información sobre la cartera entrante. Esto crea grandes brechas entre los precios de compra y de venta, ya que los vendedores generalmente no comparten suficiente información histórica para tomar decisiones de compra certeras. Un enfoque de Machine Learning para la valoración de carteras podría aprovechar los datos históricos para hacer predicciones sobre el rendimiento futuro de cada uno de los préstamos.

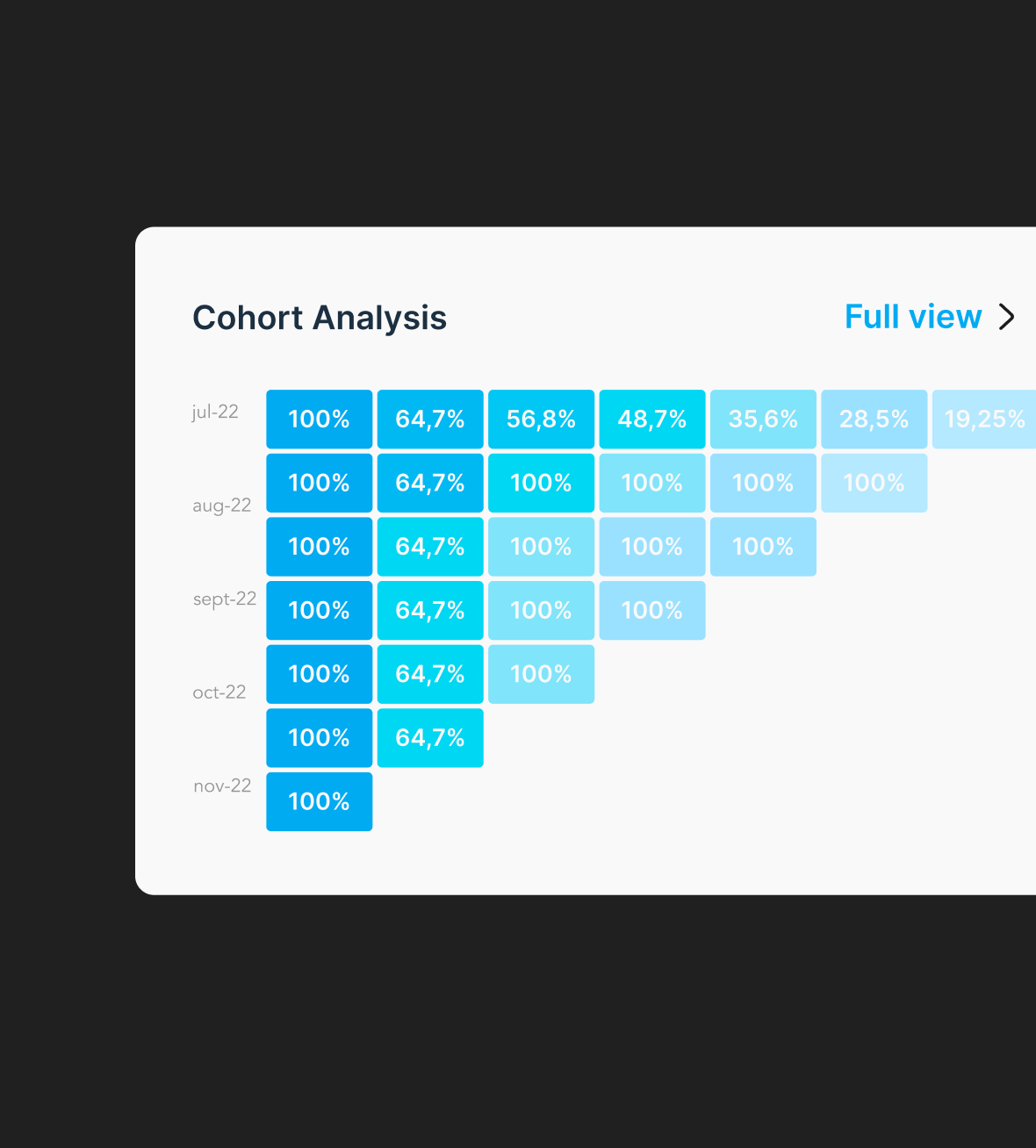

Overview

- Most NPL workout strategies are focused on manpower rather than effectiveness and efficiency.

- This generates highly inefficient workout our suite guides banks, funds and asset managers in the transformation of the Non Performing Asset into cash via different strategies.

- This generates highly inefficient workout our suite guides banks, funds and asset managers in the transformation of the Non Performing Asset into cash via different strategies.

This generates highly inefficient workout our suite guides banks, funds and asset managers in the transformation of the Non Performing Asset into cash via different strategies.

The challenge

- Most NPL workout strategies are focused on manpower rather than effectiveness and efficiency.

- This generates highly inefficient workout our suite guides banks, funds and asset managers in the transformation of the Non Performing Asset into cash via different strategies.

- This generates highly inefficient workout our suite guides banks, funds and asset managers in the transformation of the Non Performing Asset into cash via different strategies.

This generates highly inefficient workout our suite guides banks, funds and asset managers in the transformation of the Non Performing Asset into cash via different strategies.

The results

Los inversores en NPL a menudo se acercan a la compra de carteras de préstamos con poca información sobre la cartera entrante. Esto crea grandes brechas entre los precios de compra y de venta, ya que los vendedores generalmente no comparten suficiente información histórica para tomar decisiones de compra certeras. Un enfoque de Machine Learning para la valoración de carteras podría aprovechar los datos históricos para hacer predicciones sobre el rendimiento futuro de cada uno de los préstamos.

The results

Los inversores en NPL a menudo se acercan a la compra de carteras de préstamos con poca información sobre la cartera entrante. Esto crea grandes brechas entre los precios de compra y de venta, ya que los vendedores generalmente no comparten suficiente información histórica para tomar decisiones de compra certeras. Un enfoque de Machine Learning para la valoración de carteras podría aprovechar los datos históricos para hacer predicciones sobre el rendimiento futuro de cada uno de los préstamos.

Esto es un destacado del caso de éxito de tres líneas lorem ipsumEsto es un destacado del caso de éxito de tres líneas lorem ipsum.

Casos de éxito

.jpg)

.jpg)

.jpg)

.svg)

.svg)